Autonomous Pay by Link, Agent-Guided Pay by Link and Pay by Call with PBC LAA/TFA + PBC 3DS

Remote payment collection is no longer a simple choice between sending a payment link and taking a card payment over the phone.

In today’s contact center environment, three very different models coexist: Autonomous Pay by Link, Agent-Guided Pay by Link and Pay by Call with PBC LAA/TFA + PBC 3DS.

At first sight, they may appear to solve the same problem: how to collect a remote payment when the customer is not physically present. But in operational, economic, security and compliance terms, they are radically different.

The key thesis of this analysis is simple:

The optimal remote payment architecture is not based on choosing one single channel. It is based on combining channels intelligently, using each one where it reaches its maximum efficiency.

Pay by Link works well when the customer is digitally autonomous and already operating in a digital journey. But when the payment intention is created inside a phone conversation, forcing the customer to leave the call and complete the payment elsewhere can destroy conversion, increase friction and waste agent productivity.

That is the operational absurdity of channel switching.

1. The hidden problem behind Pay by Link

Pay by Link has become one of the most widely adopted tools for remote payment collection. The model is simple: the merchant generates a payment URL and sends it to the customer by SMS, email or WhatsApp. The customer opens the link and completes the transaction on a hosted payment page provided by the PSP or acquirer.

For purely digital journeys, this can be an effective solution. A customer is already browsing, receives a link, opens a secure checkout page, completes 3D Secure authentication and finalizes the purchase.

But the model becomes much less efficient when it is applied to a telephone conversation.

In many sectors, the customer’s intention to pay is not created on a website. It is created during a conversation with an agent.

This happens in debt collection, utilities, insurance, healthcare, travel, transport, public administration, subscriptions, donations and many other assisted payment scenarios. The customer may have a question, a concern, a dispute, a pending invoice, a debt, a booking or a service issue. The agent explains the situation, builds trust, resolves objections and eventually obtains a commitment to pay.

At that exact moment, the customer is ready.

But instead of closing the payment inside the same interaction, many companies send the customer a payment link and force them to leave the conversational channel.

The customer must open an SMS, click a link, trust the URL, access a mobile checkout page, enter card details, pass authentication and wait for confirmation.

Every additional step is a potential point of abandonment.

This is why Pay by Link should not be analyzed only as a payment technology. It must be analyzed as a conversion architecture.

2. A large market with structural limitations

The global payment link market is significant and growing. It has become an important part of the broader remote payments ecosystem because it offers speed, scalability and a relatively simple integration model.

However, the conversion funnel of an autonomous payment link sent by SMS contains multiple points of loss.

From 100 payment links sent, not all are delivered. Of those delivered, not all are opened. Of those opened, not all are clicked. Of those clicked, not all customers start the payment. Of those who start, not all complete the form. Of those who reach authentication, some abandon during the SCA or 3D Secure challenge. And not all authenticated attempts are finally authorized by the issuer.

The result is that, under many real-world scenarios, an autonomous Pay by Link journey may complete only around 8 to 20 payments per 100 SMS sent.

This does not mean that Pay by Link is ineffective. It means that its effectiveness depends strongly on context.

It works best when the customer is digitally confident, has a smartphone available, trusts the sender, understands the process, is comfortable with mobile authentication and has enough motivation to complete the payment without assistance.

But that is not always the reality inside contact centers.

In assisted telephone environments, many customers need support, reassurance or continuity. For them, the payment link is not a natural continuation of the journey. It is a forced channel switch.

3. Three models, not two

The remote assisted payment market is often described as a binary choice: Pay by Link versus phone payment.

That distinction is too simplistic.

In practice, there are at least three different models.

3.1 Autonomous Pay by Link

In the autonomous Pay by Link model, the company sends a payment URL to the customer by SMS, email or WhatsApp. The customer completes the transaction independently on a hosted payment page.

The main advantage is that there is no agent cost during the payment itself.

The main weakness is that the customer must complete every step alone.

This model is suitable for digitally autonomous customers and native digital journeys. It is less effective when the customer needs reassurance, assistance or channel continuity.

3.2 Agent-Guided Pay by Link

Agent-Guided Pay by Link is a hybrid practice that has become common in many contact centers.

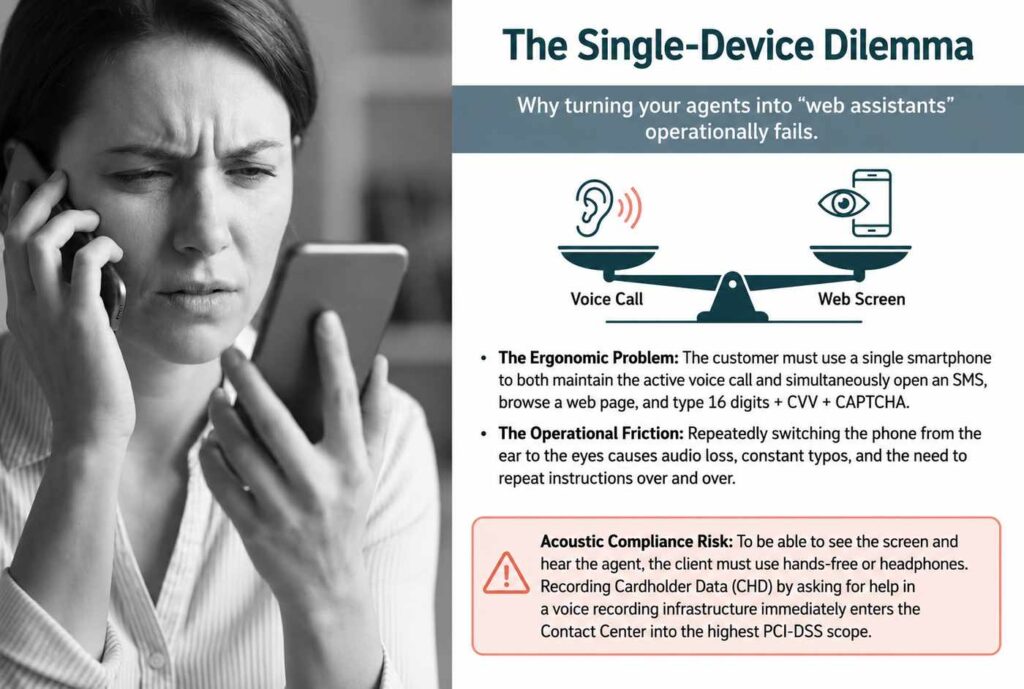

In this model, the agent sends the payment link while the customer remains on the phone. The agent then verbally guides the customer through the process: open the SMS, click the link, enter the card details, follow the authentication steps, confirm the bank message and check whether the payment has been accepted.

The agent does not handle card data directly, which may appear attractive from a compliance perspective.

However, the payment still takes place outside the voice channel.

The customer is still forced into a web journey. The agent remains on the line. The call becomes longer. The contact center consumes agent time while the customer struggles with a mobile checkout process.

This is why Agent-Guided Pay by Link is often misunderstood. It may improve conversion compared with autonomous Pay by Link, but it transfers digital friction into operational cost.

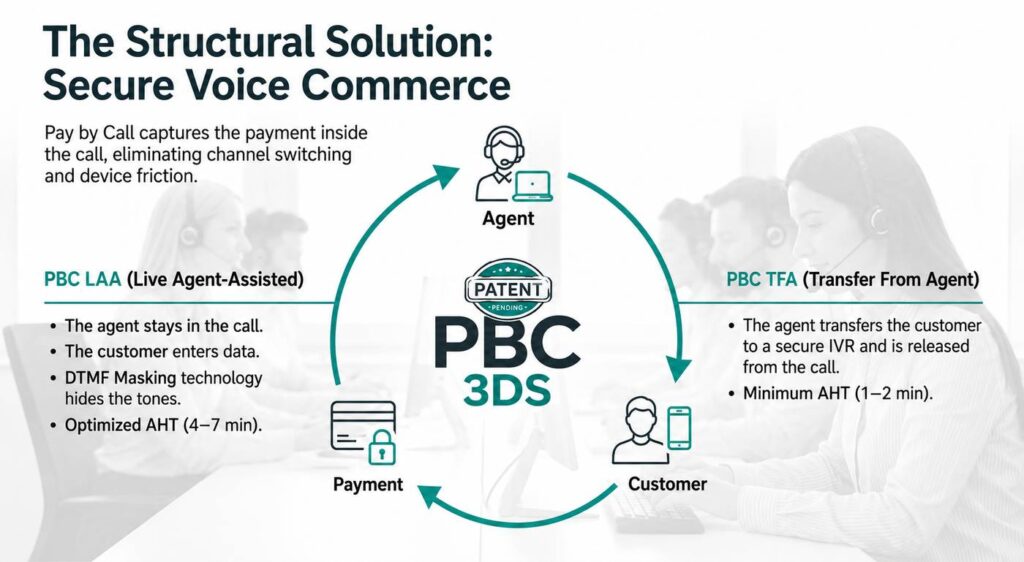

3.3 Pay by Call with PBC LAA/TFA + PBC 3DS

Pay by Call introduces a different logic.

The payment is completed inside the voice interaction, using a secure IVR environment, without exposing card data to the agent or call recordings.

With PBC LAA — Live Agent-Assisted — the agent remains on the call while the customer enters card data securely through DTMF masking in the IVR.

With PBC TFA — Transfer From Agent — the agent transfers the customer to a secure IVR at the payment moment, maximizing agent productivity.

With PBC 3DS, Pay by Call enables EMV 3D Secure 2.x inside the voice flow, without redirecting the customer to a web page.

This is not traditional MOTO. It is not an agent manually taking card data. It is not an insecure telephone payment.

It is Secure Voice Commerce: a PCIaaS layer designed to turn the voice channel into a secure, authenticated and payment-grade transaction channel.

4. The operational absurdity of channel switching

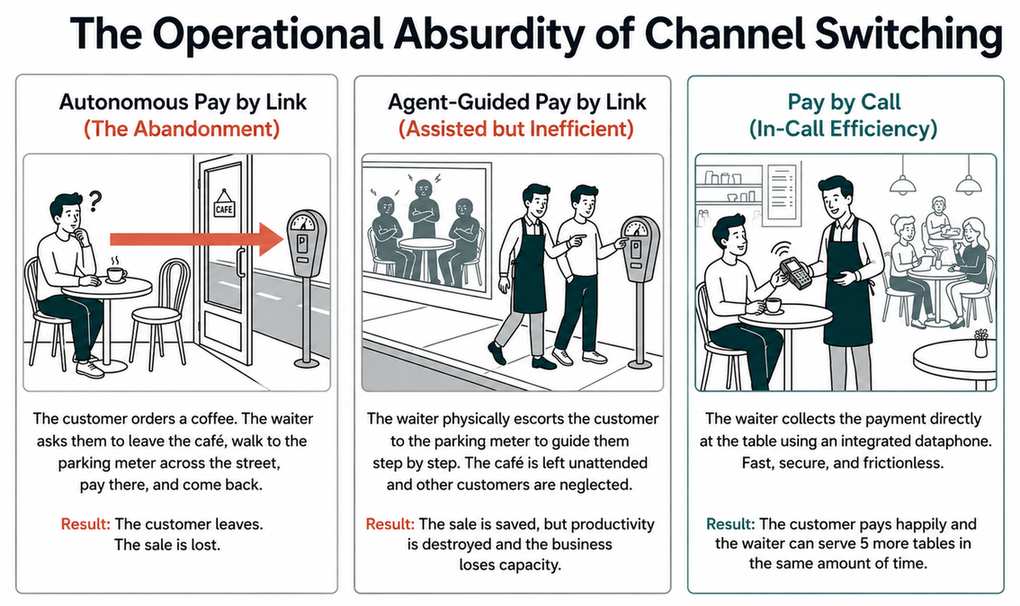

The operational absurdity can be explained with a simple analogy.

Imagine a customer sitting in a café. He orders a coffee and wants to pay. The waiter could simply bring the card terminal to the table and complete the payment there.

That is efficient. The customer pays. The waiter moves on. The business keeps serving other customers.

Now imagine that instead of doing that, the waiter tells the customer to leave the café, cross the street, walk to a parking meter, pay there and then come back.

That is Autonomous Pay by Link in a conversational payment context.

The customer may leave and never return.

Now imagine that the waiter walks with the customer to the parking meter, explains each step, waits while the customer pays, and then walks back with him to the café.

That is Agent-Guided Pay by Link.

The sale may be saved, but the waiter has abandoned the café, other tables are unattended and operational productivity is destroyed.

Finally, imagine that the waiter simply brings a secure payment terminal to the table.

That is Pay by Call.

The payment is completed where the intention was created: inside the interaction.

Fast, secure and without friction.

This analogy captures the central issue: when the customer is already engaged in a conversation, forcing a channel switch is often operationally irrational.

5. Conversion is not about links sent. It is about payments completed

Many companies measure Pay by Link activity incorrectly.

They count links sent, SMS delivered, campaigns launched or clicks generated. But the real metric is not activity.

The real metric is completed payments.

A payment channel is not successful because it sends many links. It is successful when it converts real payment intention into authorized transactions.

This distinction matters because Pay by Link often looks cheap at the attempt level but may be expensive at the success level.

Autonomous Pay by Link has no direct agent cost, but it may lose a large share of customers along the funnel.

Agent-Guided Pay by Link improves conversion but consumes agent time. If each guided payment attempt takes 8 to 18 minutes, and many attempts still fail, the real cost per completed payment can become very high.

By contrast, Pay by Call is designed to reduce abandonment by keeping the customer in the same channel where the intention to pay was created.

The right metric is therefore not:

“How much does it cost to send a link?”

The right metric is:

“How much does it cost to complete one successful payment?”

This is the KPI that contact center directors, operations managers, collections teams and CFOs should analyze.

6. Agent-Guided Pay by Link: a hidden cost center

Agent-Guided Pay by Link is often presented as a compromise between security and assistance.

The agent does not take card data, and the customer is not completely alone. This may sound like a good balance.

But the model has a structural flaw: the agent remains trapped inside a payment journey that the customer must complete outside the voice channel.

The agent waits while the customer searches for the SMS.

The agent waits while the customer opens the link.

The agent waits while the mobile page loads.

The agent waits while the customer enters card details.

The agent waits while the bank authentication is triggered.

The agent waits while the customer tries to approve the payment.

The agent waits when the process fails.

In a high-volume contact center, this is not a minor inconvenience. It is an operational cost.

Agent time is one of the most expensive resources in a contact center. Using that time to guide customers through a mobile checkout process is inefficient when a secure in-call payment architecture can complete the transaction inside the same conversation.

The agent’s highest value is in explaining, negotiating, solving objections and creating trust. Once the customer agrees to pay, the architecture should allow the payment to be completed with minimum friction and minimum agent time.

That is precisely the role of Pay by Call.

7. Security, fraud and trust

Pay by Link can be technically secure when the payment takes place on a PSP-hosted page with 3D Secure authentication. But the security of the payment page does not solve all the risks of the customer journey.

The customer receives a link. That link competes with a growing number of phishing and smishing attempts. Even when the link is legitimate, the customer may hesitate.

Is this message real?

Is this URL safe?

Is this really my utility provider, insurer, airline or public authority?

This loss of trust affects conversion.

Smishing and phishing have trained consumers to distrust payment links. For sectors that rely on customer confidence, this is a serious problem.

In Agent-Guided Pay by Link, the link still exists. The customer still receives it. The payment still moves to a web environment.

Pay by Call removes this specific risk because the customer does not need to click a payment link. The payment is completed inside the call through a secure IVR environment.

Card data is not exposed to the agent.

Card data is not captured in call recordings.

The contact center reduces PCI DSS exposure.

And with PBC 3DS, the transaction can include strong customer authentication within the voice flow.

This creates a fundamentally different security architecture.

8. PCI DSS 4.0.1 and the compliance dimension

Compliance is becoming a decisive factor in remote payment architecture.

PCI DSS 4.0.1 introduces stricter requirements for merchants using payment pages that involve iframes, JavaScript and browser-based integrations. Depending on the technical model, this can expand compliance obligations significantly.

In contrast, a secure voice payment architecture with DTMF masking and a PCIaaS model can help keep the contact center environment out of scope for sensitive card data.

This is particularly important for large organizations, BPOs and public sector entities, where compliance complexity can become a major operational burden.

Pay by Call’s proposition is not to replace the customer’s PSP or bank.

It is to act as a secure technological layer between the contact center, IVR, BPO, telephony environment and the existing PSP.

In other words, Pay by Call does not compete with the payment ecosystem already in place.

It complements it.

It provides a PCIaaS layer for secure voice payments, allowing organizations to maintain their current acquiring relationships while adding a specialized secure execution layer for the voice channel.

9. Why PBC 3DS matters

One of the key limitations of traditional voice payments has been the difficulty of bringing strong authentication into the voice channel without forcing the customer into a web redirection.

PBC 3DS changes this logic.

It enables EMV 3D Secure 2.x execution inside the IVR voice flow, without redirecting the customer to a browser-based payment page.

This matters because it aligns the voice channel with the security expectations of e-commerce while preserving the conversational experience.

For merchants, this opens the door to stronger authentication, better fraud protection and a more modern compliance posture.

For customers, it reduces friction.

For contact centers, it creates a way to close payments securely without exposing card data or forcing customers into a channel switch.

This is the core of Secure Voice Commerce.

10. Use cases where voice has structural advantage

The superiority of one payment channel over another is not absolute. It depends on the operational context.

However, several sectors show a clear structural advantage for secure assisted voice payments.

Debt collection

In debt collection, payment often follows negotiation. The customer may need to understand the amount, agree on a plan or resolve a concern. Once the customer accepts, the payment should be closed immediately. Sending a link at that moment risks losing the commitment.

Utilities

Utility payments are often urgent. Customers may be trying to avoid service interruption, regularize overdue invoices or resolve billing issues. Many customers also include elderly or digitally vulnerable segments. Voice continuity is critical.

Insurance

Insurance customers may require identity verification, reassurance and support. Secure voice payment can reduce friction while supporting customers who are less comfortable with digital forms.

Travel and hospitality

Travel bookings, changes and urgent reservations often happen under time pressure. If a customer is already on the phone with an agent, completing the payment in-call can protect conversion.

Public administration

Public sector payment journeys must consider accessibility and digital inclusion. Not every citizen can or wants to complete a payment through a mobile link. Secure voice payments can support a more inclusive model.

Healthcare

Healthcare payment interactions may involve vulnerable patients, sensitive contexts and the need for assisted support. A secure in-call model can improve both trust and completion.

Donations and non-profit campaigns

Emotional urgency matters. When a donor commits during a call, sending them away to a link may reduce conversion. Completing the donation inside the interaction can be more effective.

11. Inclusion: omnichannel does not mean forcing everyone into digital self-service

One of the most overlooked dimensions of payment architecture is inclusion.

Not every customer is digitally autonomous.

Not every customer trusts SMS links.

Not every customer can navigate a mobile checkout page easily.

Not every customer has the same level of confidence with banking authentication.

Digital transformation should not mean forcing every customer into the same channel.

True omnichannel architecture means offering the right channel for the right context.

Autonomous Pay by Link for digitally confident customers.

Agent-Guided Pay by Link as a transitional model where needed.

Secure Voice Commerce when the customer’s payment intention is created inside a conversation.

This is not about defending old channels. It is about designing better payment journeys.

The voice channel is not a legacy channel when it is used correctly. It is a high-intent channel.

And high-intent channels deserve payment-grade execution.

12. From payment channels to payment architecture

The market needs to move beyond isolated payment tools.

A payment tool answers a tactical question:

“How can I collect this payment?”

A payment architecture answers a strategic question:

“How can I convert payment intention into completed payment with the least friction, lowest risk, strongest compliance and best operational efficiency?”

That distinction is crucial.

Pay by Link should not disappear. It should be used where it performs best.

Agent-Guided Pay by Link should be understood for what it is: a hybrid operational workaround that may help in certain cases but can become expensive at scale.

Pay by Call should be deployed where the conversation is the source of trust, context and payment intention.

The future is not one channel replacing another.

The future is intelligent orchestration.

13. Secure Agentic Voice Commerce: the next frontier

The relevance of this debate increases as the market moves toward Agentic Commerce.

AI agents will increasingly help customers discover products, compare options, initiate purchases and interact with companies. Banks, PSPs, card schemes and technology platforms are already exploring agentic payment models.

But one question remains underdeveloped:

Where will the payment be executed securely?

If the intention is created in a conversation —with a human agent, an AI agent or a hybrid model— the payment layer must be secure, compliant and payment-grade.

General-purpose AI should not handle sensitive card data directly.

Conversational AI should be able to hand over the transaction to a secure execution layer.

That is where Secure Agentic Voice Commerce becomes strategically important.

Pay by Call can act as the PCIaaS execution layer for voice-based and conversational payment flows, ensuring that the AI-driven experience remains outside the sensitive PCI perimeter while the actual transaction is executed inside a secure environment.

This is not only about today’s contact centers.

It is about the future architecture of conversational commerce.

Conclusion: the right channel in the right context

The debate should not be framed as Pay by Link versus Pay by Call.

The real question is:

Where does each channel create the highest conversion, lowest friction and best operational efficiency?

Autonomous Pay by Link is useful when the customer is digitally autonomous and the journey is already digital.

Agent-Guided Pay by Link may be useful as a transitional model, but it must be analyzed carefully because it can hide significant agent costs.

Pay by Call becomes structurally stronger when the intention to pay is created inside a voice conversation and when forcing the customer to switch channels damages conversion.

The optimal architecture does not replace channels.

It combines them intelligently.

Digital links for digital journeys.

Human assistance for trust and negotiation.

Secure IVR for sensitive card data capture.

The existing PSP for payment processing.

A PCIaaS layer for compliance.

And PBC 3DS for strong authentication inside the voice channel.

That is the real shift: moving from isolated payment tools to an integrated remote payment architecture.

Because the metric that matters is not how many links are sent.

It is how many real payment intentions become completed, authenticated and secure transactions.

And when that intention is born in a conversation, the voice channel is not the past.

It may be the most efficient place to close the future of secure remote payments.