Agentic Commerce is no longer a distant concept. It is becoming one of the most important conversations in the payments industry.

Payment networks, banks, PSPs, technology platforms and AI companies are all preparing for a new environment in which artificial intelligence agents will not only help users search for information or compare products, but also participate in decision-making and payment execution.

This evolution makes sense. If users increasingly delegate part of their purchasing decisions to AI assistants, digital commerce will have to adapt. It will no longer be enough for a website to be well positioned in search engines or for a checkout to be optimized for human navigation. Product catalogues, commercial conditions, authentication flows and payment processes will have to become accessible, understandable and executable by intelligent agents.

But there is a risk in the current narrative: confusing a good demonstration with the real market.

Many early examples of Agentic Commerce are built around simple retail scenarios. An AI agent buys a T-shirt, a pair of shoes or a low-risk consumer product in a perfectly controlled digital environment. The user expresses a need, the agent searches for options, compares prices, selects a product and completes the purchase.

As a demonstration, it works.

As a representation of the real challenge ahead, it is incomplete.

Because the future of commerce will not be determined only by proving that an AI agent can buy a T-shirt in a perfect retail checkout. The real challenge will be executing real transactions, in real contexts, with real constraints, in sectors where customer intent already exists and where payment is not a trivial action, but a critical part of the relationship between a company and its customers.

This is what we can call the Agentic T-Shirt Problem.

The industry is using low-friction retail purchases to demonstrate a paradigm whose greatest value may emerge in high-friction, high-intent and high-volume service transactions.

Buying a T-shirt is easy.

Real commerce is not.

In the real economy, many transactions do not begin with a user casually browsing a catalogue. They begin when a customer needs to pay a utility bill before a service is interrupted. When a traveller calls to change a booking and pay a price difference. When a citizen contacts a public administration to pay a tax, fee or fine. When an insurance customer renews a policy. When a patient confirms and pays for a healthcare service. Or when a debtor reaches a payment agreement during a live conversation.

These are not marginal use cases. They are part of the daily operation of large sectors such as utilities, public administrations, travel, insurance, healthcare, debt collection, contact centers and BPOs.

And in many of these environments, commerce does not begin with discovery.

It begins with intent.

The dominant narrative around Agentic Commerce focuses heavily on the ability of AI agents to discover, compare, recommend and decide. That matters. But in many sectors, the customer does not need an AI agent to create the intent. The intent is already there.

The customer already knows there is something to pay.

The customer already needs to resolve an issue.

The customer is already interacting with the company.

The customer has already expressed a willingness to act.

In many cases, the amount is already known.

In that context, the real challenge is not generating intent. The real challenge is executing it securely.

And this is where a channel that has often been treated as old, secondary or inconvenient becomes strategically relevant again: voice.

Voice is frequently described as a legacy channel. But that view confuses age with irrelevance. Voice remains important because it continues to solve situations where a website or an app is not always enough. Some transactions require assistance, trust, explanation, urgency, negotiation or human support.

When a customer calls a utility company, an airline, an insurance provider, a public administration, a hospital, a contact center or a debt collection operation, they are usually not browsing. They are trying to resolve something.

From a commercial perspective, this moment is extremely valuable. The intent is declared. The context is present. The conversation is active. The willingness to complete the transaction already exists.

Yet voice has historically remained disconnected from much of the innovation that has transformed digital payments.

The problem is not conceptual. It is infrastructural.

For years, strong customer authentication — especially through mechanisms such as 3D Secure — has been mainly associated with screen-based experiences. As a result, telephone and IVR payment environments have often been treated as difficult to integrate into native strong authentication flows.

The usual response has been to move the customer outside the conversation.

Send a payment link.

Ask the user to open an SMS.

Move the payment to a screen.

Complete the transaction in another channel.

Then, in many cases, return to the call to confirm the result.

Pay by link has been useful because it solved a specific problem: removing card data from the agent or contact center environment. But it also created a break at the most delicate moment of the journey: precisely when the customer has already declared intent and is ready to pay.

In other words, the card data is protected, but the experience is interrupted.

That interruption will become increasingly difficult to justify in a world moving toward conversational interfaces, AI assistants and hybrid human-agent journeys. If the conversation is where intent is created, clarified or confirmed, why should the customer be forced to abandon that conversation at the exact moment of payment?

This is one of the major questions Agentic Commerce will have to address.

Because Agentic Commerce cannot be reduced to discovery or recommendation. The critical question will not only be what an AI agent can find. The critical question will be what the agent is authorized to do, who gave that authorization, how it is verified, how the transaction is authenticated, how it is audited, who assumes liability and how the whole process integrates with existing payment infrastructure.

In real commerce, execution is not a trivial extension of intelligence. It is a separate layer defined by authentication, authorization, traceability, compliance, liability and security.

That is the real bottleneck.

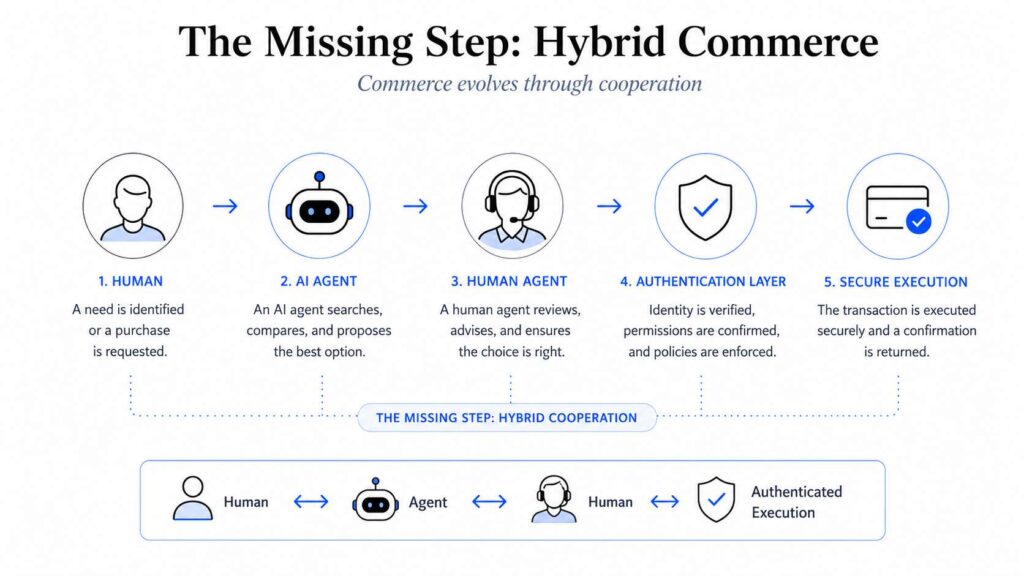

This is also why the natural path will not necessarily be an immediate jump into fully autonomous agent-to-agent commerce. Before that, there will be a much more immediate and probably much more commercially relevant phase: hybrid commerce.

A human assisted by AI.

An AI assistant supported by a human.

A human agent enhanced by artificial intelligence.

A conversational assistant guiding a transaction.

A user confirming intent.

A secure authentication process.

A payment executed within the same flow.

This hybrid phase should not be seen as a minor transition. It is the natural bridge toward real Agentic Commerce.

In sectors such as utilities, travel, insurance, healthcare, public administrations, debt collection and BPOs, this stage can be deployed much earlier than many futuristic scenarios of fully autonomous commerce.

The infrastructure already exists.

Customers already call.

Agents already assist.

PSPs already process.

Acquirers already settle.

Companies already manage customer service, renewals, bookings, collections and assisted payments.

What is missing is a secure layer that connects conversational intent with authenticated payment execution.

At Pay by Call, we believe this is where a new category begins to emerge:

Secure Agentic Voice Commerce.

This is not simply telephone payment. It is not just IVR. It is not pay by link. And it is not merely Agentic Commerce applied to retail.

Secure Agentic Voice Commerce is the layer that connects conversation, intent, authentication and secure payment execution inside the voice channel.

Its defining characteristic is simple but important: the transaction can be completed within the conversation, without forcing the customer to abandon the channel at the precise moment they are ready to pay.

This approach will be especially relevant in sectors where voice remains critical for high-value, high-complexity or high-sensitivity transactions. It will also matter wherever user experience, conversion and continuity of the call are essential.

This is precisely the problem Pay by Call addresses with PBC 3DS, our international patent-pending method designed to enable native 3D Secure authentication in telephone and IVR payment environments, without forcing the user to leave the voice channel.

PBC 3DS is designed to remove one of the historical limitations of telephone payments: the difficulty of integrating strong authentication without pushing the customer into an external screen-based experience.

The difference is significant.

This is not only about allowing a customer to pay by phone. It is about making it possible for intent expressed in voice to become authenticated, traceable and secure execution within the same conversational flow.

And it does so without requiring companies to redesign their existing payment infrastructure.

Pay by Call acts as a technology layer for security and compliance — a PCIaaS, Compliance-as-a-Service model — that can integrate with contact centers, BPOs, IVRs, conversational AI assistants, PSPs and acquiring banks.

The objective is not to replace the existing payments ecosystem.

The objective is to make it more powerful for the voice channel.

That is why the agentic T-shirt is a good demo, but it should not become the center of the debate. The real opportunity lies elsewhere: bill payments, renewals, bookings, taxes, debt collection, assisted customer service, contact centers and transactions where the customer is not browsing, but trying to resolve something.

It lies in conversations where intent is already declared.

It lies in moments where leaving the channel can mean losing conversion, trust or continuity.

An AI agent buying a T-shirt may help explain the concept of Agentic Commerce. But it does not represent its full potential.

The real market will be about connecting verifiable intent with authenticated execution.

If Agentic Commerce is to mature, it must move beyond controlled demos. It must enter sectors where real constraints exist: compliance, authentication, user experience, integration with existing infrastructure, traceability, liability and security.

The question is no longer whether AI agents will participate in commerce.

They will.

The real question is who will connect this new layer of intelligence with a secure execution layer. Who will enable payments inside conversational flows. Who will make strong authentication compatible with voice. Who will turn Agentic Commerce into something operational for the real economy.

At Pay by Call, we believe the answer begins with Secure Agentic Voice Commerce.

Because the future of commerce will not be won by proving that an AI can buy a T-shirt in a perfect checkout.

It will be won by executing real transactions, in real contexts, with real customers and with all the guarantees of security, authentication and compliance.

And in many of those contexts, the channel is still voice.

Secure Agentic Voice Commerce is not a distant evolution of Agentic Commerce.

It is the layer that can make it operational.